Richard Rosso.

The bond markets are downright spooked. Or are they??

It all depends on your perspective.

How much media hype can you absorb (and believe me there’s a feeding frenzy going on in the financial media) without running from bonds like victim trying to fruitlessly escape from “Leatherface,” the psycho killer in “The Texas Chainsaw Massacre.”

You cannot escape!

You cannot escape!

What is a bond? Well, boys and girls a bond is a debt. You loan money to a corporation, a government, a municipality and for that you privilege you receive interest payments (income) and eventually, if the borrower is high quality, you’ll receive your original investment back (no this not like lending to your brother-in-law). And when interest rates go up, your bond may be worth less (if you try to sell it before it matures). Most important, when interest rates rise…..

IT’S THE END OF THE WORLD FOR BONDS!!!!

Look! A bonderoid just hit!!!

Look! A bonderoid just hit!!!

You would think we’re smack in the middle of the zombie apocalypse and bonds are biting and infecting portfolios. It’s World War B! (Sorry Brad Pitt I stole your cinema thunder for WWZ, coming to a theatre near you, soon).

Look there’s a zombie cat in World War Z!!!

Look there’s a zombie cat in World War Z!!!

So, let’s take a breath and examine this situation with level heads, shall we? Master Blogger, best-selling author, friend James Altucher advises readers, followers, to take deep breaths and hold for 4 seconds (or 4 ticks in the 10-year Treasury note yield).

Ok. Are we relaxed? Let’s get excited again!

Because..

OMG OMG OMG OMG!!! (MEDIA UNCUT INTERPRETATION).

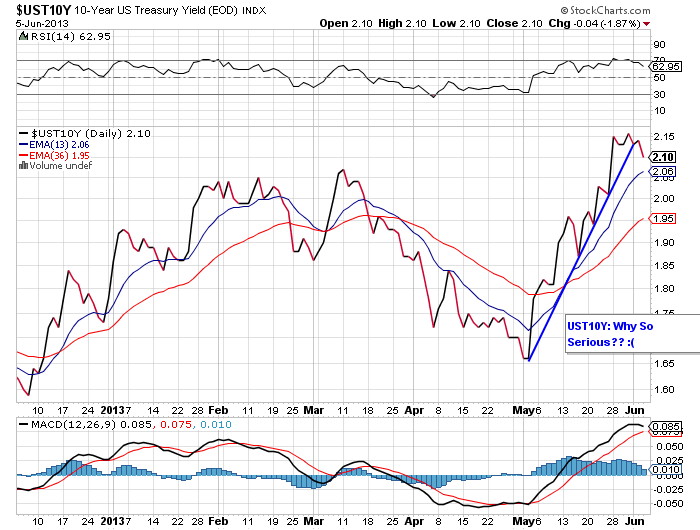

Yes, is the short-term whoosh a bit unnerving in treasury yields? Sure. Most troubling, as bond prices were falling (due to rising interest rates), stocks were faltering too, especially the more “interest-rate” sensitive groups like utilities, MLPs, REITs. Overall, every asset class experienced a respectable pummeling.

The positive connection was a bit scary as I have diversification phobia. Based on research and observation, true diversification has become a challenge, especially since the financial crisis. As I’m paid to help clients reach personal financial benchmarks and manage portfolio risks, I’m a forever student on this topic.

Despite what you hear from the financial services industry, diversification is not some form of panacea. Yes, it’s important, however true diversification is becoming tougher to achieve these days. So, when bonds don’t provide diversification to the movements in stocks, it brings back night sweats circa 2008.

Some of my research for my second book leads me to the mysterious topic of diversification. Reading takes me back to the 1920’s: 1920-1929. From the writings of stock market sages long dust in the ground. From the defunct but once iconic “The Magazine of Wall Street.” Featured briefly in the recent remake of “The Great Gatsby.” Those movie people sure do their homework! I was shocked by the authenticity.

Here’s a meaty excerpt from October 23, 1926 I thought you’d enjoy:

“Diversification in securities is an art understood only by a few (comment: nice to know nothing’s changed) but remains prime necessity if the investor is to gain the greatest degree of safety without sacrificing the possibility of profit. To spread one’s cash among a number of different issues is not necessarily diversification.”

Strange. I’ve asked a few brokers what they believed diversification was and received the response: “To spread one’s cash among a number of different issues.” Hmm.

I miss you, 1926.

Stay with me. Hold the line.

“To diversify properly, it is necessary that a certain portion be allotted for safe-keeping and another portion for income and profit producing.”

I like that. So when bonds and stocks begin to move in the same direction, it causes me to sweat just a bit, become more aware of the macro conditions (mostly sweat).

Oh, where were we? Oh right: The move in bond yields.

And we have been deep-breathing, correct?

So. Oh yeah.

OMG OMG OMG OMG! Let’s think a bit longer term, shall we?

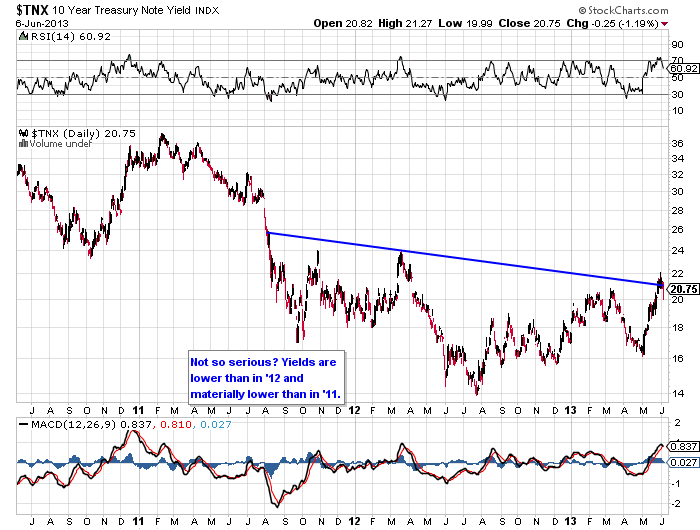

Yields are still lower than 2012, and even lower than 2011. Whew. Perhaps the sell-off was/is an overreaction. You mean we overreact in the bond markets now too? Sheesh!

I can hear the cry now: Has Ben Bernanke abandoned us?

Awww, heck no!!!

Awww, heck no!!!

Now, now dry your eyes. Let’s review why BB is still supportive of risk assets and bonds are not as terrifying as everybody seems to believe:

1). First unemployment is nowhere near the Fed’s target of 6.5%. And based on past interest rate action higher or lower, we know that the Fed moves like an aged Fed Governor’s gait on ice. My favorite chart by Bill McBride shows how far the economy still needs to go before we even reach peak employment (pre-financial crisis). It’s like 62 months already. Is the situation improving? Yes. Slowly. However, the bond market is reacting like the economy is ready to reach escape velocity and we’re going to see major hiring right around the corner. It’s all about aggregate demand, stupid. And speaking of such.

According to the BLS (the Bureau of Labor Statistics):

Within leisure and hospitality, employment in food services and drinking places continued to expand, increasing by 38,000 in May and by 337,000 over the past year.

Retail trade employment increased by 28,000 in May. The industry added an average of 20,000 jobs per month over the prior 12 months. In May, general merchandise stores continued to add jobs (+10,000).

Health care employment continued to trend up in May (+11,000). Job gains in home health care services (+7,000) and outpatient care centers (+4,000) more than offset a loss in hospitals (-6,000). Over the prior 12 months, job growth in health care averaged 24,000 per month.

So, if my math is correct 94,000 out of the 175,000 jobs created in May were in lower-paying industries of the economy.

My favorite waitress at Cracker Barrel restaurant, Jessie Lou, does a great job. I’m certain she consumes. I know I’m a good tipper too. That doesn’t mean Jessie Lou has a lot of spending power. I’m thinking Ben Bernanke is examining the quality of the underlying jobs too before he decides to alter his actions.

2). Households are still deleveraging. A fancy way of saying they’re paying down debts. They’re not maxing out credit cards or using their houses as ATMs anymore. You see, corporations can shore up their balance sheets relatively quick, in a few quarters. It’s not the same for households. It takes time for household balance sheets to heal. Progress is happening. We’re just not there yet. I mean what are you gonna do? Fire the kids to lower expenses? No. You spend less (see below).

3).Nobody rings a bell, blows a whistle, no Paul Revere stuff happens when it comes to the reduction of a bond buying program. A metric doesn’t exist which helps markets gauge when the Federal Reserve decides to “taper” or stop their grand experiment so markets attempt to decipher what Bernanke says and then overreact to the overreaction.

Even when BB is crystal clear about his intentions, traders, investors, the media are seeking the meaning behind the meaning and taking out their guesses on stock and bond prices. Tell me if you heard this – If the economic news is bad that means the stock market will like it and head higher. If the news is really good that’s good too because that’s a signal that the Fed can unwind gracefully. Huh? Frankly, all of us involved with investments are guessing at best.

There’s no way to judge how the Fed extracts from this zero/low interest rate experiment but believe me the world is watching. It’s like taking a shower with the curtain open and having all the heads of global central banks sitting on the bathroom floor watching, waiting.

It all reminds me of one of my favorite games as a child – The Milton Bradley classic – “Operation.”

With a skilled hand you use tweezers to reach into “patient Sam” and extract all types of hilarious body parts – Adam’s Apple, Butterflies in the Stomach (a plastic butterfly), Spare Ribs.

Now the challenge is the plastic ailments are tiny. The openings within “Sam” are slim, so you must go in and extract without touching the metal edges of the openings with the tweezers, otherwise a loud buzz goes off and Sam’s red nose lights up like a Christmas bulb.

Right now, Bernanke has the tweezer on the Funny Bone and if he doesn’t use a steady grip to extract, he’s going to set off the buzzer on panic and stock, bond markets will light up red. Not an easy feat (and it won’t be funny). Appears BB has a real dilemma on his hands.

Markets will remain volatile and trade off headlines as we go through summer.

What to do?

FIRST, DON’T PANIC!!

Now..

1). Decrease your bond durations to 3-5 years. In other words, speak to your broker, adviser and have them decrease the interest rate sensitivity in your bond portfolio. Investors are not going to totally abandon bonds but we are going through a re-evaluation of bond yields which will drive you crazy.

4). Dividend-based and interest-rate sensitive stocks are beginning to look attractive again. For example, the exchange-traded fund XLU, which holds, well, S&P utility stocks, has worked off an overbought condition. I’m waiting for a positive MACD crossover before I enter. As of the close of business on Friday, June 7, the twelve month yield is 3.86% according to Morningstar.

Overall, we live in interesting times and our grand interest rate suppression experiment will make history.

For now, all we can do is breathe.