Don’t kid yourself. The Fed affects everything when it comes to your money.

As I wrote previously, it was highly unlikely the Fed was going to pull back on purchasing $85 billion in Treasury and Mortgage bonds in September.

Because:

“Mom, I just saw Ben Bernanke!”

“Mom, I just saw Ben Bernanke!”

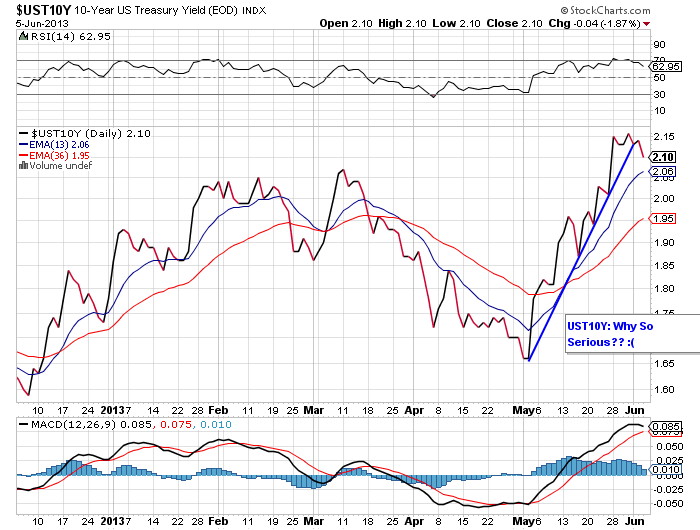

Have you checked the volatility in mortgage rates lately? The 30-year fixed breached 5% and now has backed off. How about activity? New-home sales are nowhere near pre-crisis recovery levels.

Wall Street and large investors have swallowed up existing homes which has spiked housing inflation, making them less affordable for home buyers like you and me. Ben Bernanke is clearly concerned about the overall state of the housing market which leaves him frozen to move away from the great experiment.

How would you feel about a higher interest rate on an auto loan or credit card? We’ve seen anywhere from a 4-10% decrease in median real incomes since 2008, for American families. Part-time employment is the new full time job. Anyone believe the Fed wants to weaken your shaky household balance sheet by creating monetary uncertainty in the face of inept fiscal policy?

Have you checked the anemic interest you receive on savings accounts and money markets? It’s a bad joke. And what about the portfolio? There’s an impact due to interest rate policy.

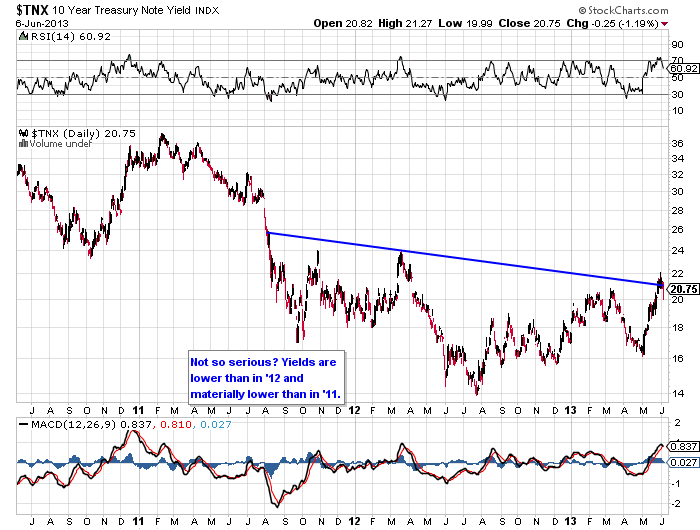

There’s a big ka-pow to the pocket and economic activity if rates continue to increase rapidly too, as they’ve done recently.

Brett Arends’ article about rising interest rates for MarketWatch was an eye-opener. Don’t blink: Click to read:

How the Fed can cause another 1987 crash.

As a student of the Great Depression, the last thing Ben Bernanke wants to do is create a 1937 like Fed hubris-induced market crash.

Higher rates matter. You’re smart enough to know that. So, what won’t your broker tell you about what looks like an imminent conclusion to the Federal Reserve’s grandiose bond-buying experiment? And what if the Fed puts off a taper as far out as 2015? It could happen. How will investors deal with the volatility?

Bonds are supposed to be the “safe” money, but is it?

What do you need to know to make you a smarter investor?

1). Cash is an asset class. No, it is. Really. Cash doesn’t gyrate. It provides protection when stocks and bonds are both heading south. Like now. Cash is a stabilizer. Think of it as the foundation under your house. Just because it’s not pretty and doesn’t feel like it’s doing much, realize it has an important job: To provide stability. Cash is a good diversification tool. It doesn’t zig, zag. It just sits there. Like an anchor. Think of cash as an anchor. Or a Snuggie.

Remember the Snuggie?

They “jumped the shark” with the doggie Snuggie.

They “jumped the shark” with the doggie Snuggie.

Your broker would prefer all your money is invested regardless of prices paid for the investments. Having cash takes discipline. A portfolio strategy would be nice so there’s an ongoing plan to put cash to work. Having cash won’t burn a hole in the portfolio. Eventually you’ll invest it. What’s the rush? Well, maybe you won’t since there’s nothing wrong with maintaining a targeted amount of cash in your asset allocation at all times.

From my own past experience I was advised by a “concerned” branch manager, that I held “too much cash” in client portfolios. I had ten percent across the board. You would have thought I committed murder. Ask your financial person: How much cash should I maintain?” Let me know when you get the blank stare, open mouth. Drooling.

2). I don’t have time to help you rebalance, I have a sales quota. Your broker’s main job is to sell. Then it’s pack you up and move you on to a place I call “no-rebalance land.”

Rebalancing is important at all times and especially important now. It’s a strategy to sell high, buy low. It’s also effective at managing portfolio risk over time.

Ask your broker – “What kind of rebalancing process is right for me now that interest rates are rising and stocks are off their highs?” I expect you to be met with more glazed eyeballs.

3). I’m relationship on the surface, transactions underneath. I was warm and fuzzy months ago when I sold you that fixed income investment. I’ve been out to lunch ever since.

Have you received a call from your broker to talk it out, gain knowledge about the current environment? Perhaps there’s nothing you need to change when it comes to your bond or fixed income allocations. It would be nice to know, wouldn’t it? A little reassurance and education can go a long way.

Leave a message. Your broker will get back to you.

4). I stink at understanding you from a behavioral perspective. I’m not a shrink, I’m a sales person. So many studies exist which outline how humans are not wired to place money into bonds, stocks, gold, widgets. Our brains are like primal beasts when it comes to investing. We are prone to emotional reaction (or overreaction), fear & greed, selling low, buying high.

We are our own worst financial enemies. Can your broker provide perspective? Odds are not good. It’s time for a good read. From Wall Street Journal writer Jason Zweig. He’s smart about this psychological money conundrum we all face. Here you go:

5). I don’t study on my own. I depend on a corporate think tank to feed me thoughts. This isn’t all bad. There are smart investment strategists out there. However, it would be refreshing if your broker had his or her own opinion about a macroeconomic event even if it conflicts with the corporate brain feeder.

A good broker will lay out the risks, rewards, pros and cons. Try this: “Forget what your company thinks about this interest rate train-wreck – What are YOUR thoughts?” I’m really setting you up for disappointment. I’m sorry.

6). I have no idea how Fed actions affect your portfolio long term. If you hear these words, keep your broker. He or she is a gem. Frankly, even during the Great Depression, interest rates were never this low for so long.

7). I have no thought-out rules to manage risk the Fed has created. First, to manage risk in your bond portfolio, shorten what’s called your bond portfolio duration (a measure of interest rate sensitivity) now. As prices have recovered in the face of a Fed “fakeout” or no taper, you now have an opportunity to re-position your fixed income allocation.

Currently, our portfolios are roughly 3-4 years in duration making them less sensitive to future increases to interest rates. We hold a targeted amount of risk in emerging markets bonds which possess attractive yields (4-5%). Municipal bonds are also priced attractively even for those in lower tax brackets.

Second, we are in the process of liquidating all GNMA investments – if interest rates increase again, refinancing activity will drop off which can lengthen a GNMA bond’s time frame to payoff or maturity. Longer time frames can result in greater principal risk or lower returns to current bondholders.

Third, we have created a series of duration-reduction rules based on our study of the long-term trends in Treasury yields. Currently, a 10-year Treasury yield of 3.15-3.25% would warrant attention and perhaps a reduction of bond durations to 2-3 years.

The unwind from this Fed experiment is beyond comprehension – there’s no historical precedent.

Make sure your adviser is at least searching for, inquiring about, gaining information from others who are smarter. Your financial partner needs to be flexible enough to change up your fixed income strategy if warranted.

Honesty, study and communication are the keys to make it through this period.

My thought? The Fed will not taper in 2013. However, the volatility in yields will remain as all of us cling to every word, each media bite out of Federal Reserve officials and then take action.

Overreactions will be the norm.

And you thought bonds were supposed to be the “boring” slice of your portfolio.

Don’t panic. Keep your cool.

Oh, and call your broker.