In the AMC’s hit drama “The Walking Dead,” where the world is overrun by rotting corpses with a desire to feed on the living, there’s something even greater to fear.

The survivors.

Staying alive in a post-apocalyptic society appears to bring out the worst of what’s left of humanity. People are ruthless killers. Strength in numbers is the best defense, yet poses an interesting dilemma.

One wrong move, one bad decision, and you’re history.

Just like that.

Sometimes, overcoming the most complicated of challenges comes down to the obvious. Nothing’s perfect however complexity fosters confusion which can shift focus, divert your attention. And when your enemies, especially within, outnumber you, it’s only a matter of time before.

Well. You know (it isn’t good).

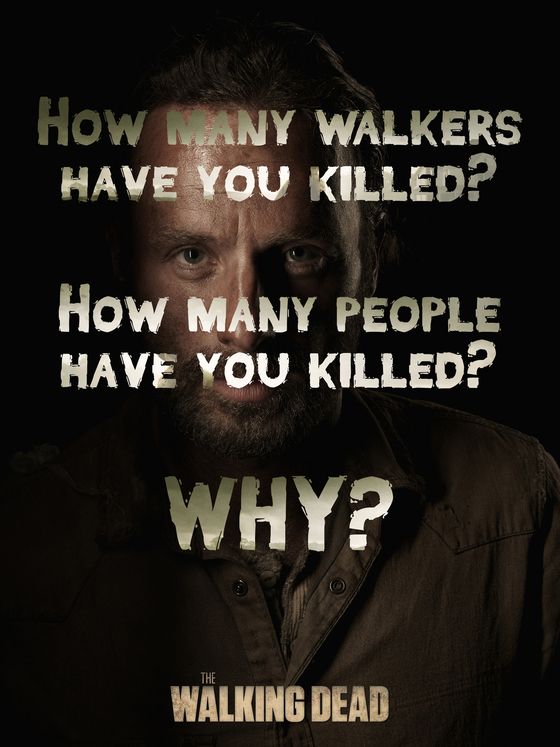

The good guys devised a simple screening method.

An initial shield to determine if strangers they encounter are worth entry into their community.

Three questions.

Let’s see how you do. Will you pass or fail?

Are you team material?

Or are you best left alone to fend for yourself?

How many walkers (corpses with an appetite for the living), have you killed?

To safeguard others, a survivor must be willing to take out the undead (a shot or blow to the head does it). Plain and simple. If your zombie kills are minimal or non-existent there will be doubts about your contribution to the survival of the group.

How many people have you killed?

Unfortunately there are instances when tough decisions must be made for the sake of self-preservation. Best the number of walkers taken out exceed the number of people otherwise you may become a victim yourself.

Why?

Tread carefully. The reasons for taking out the living best be because of personal survival. Or request. You see -There are sad instances when victims of zombie bites would rather die honorably, in their control, rather than expire from the disease they carry.

They would rather not wake up. Walk around.

As I ponder the power of simple questions, whether in fact or fiction, I have come to realize how most situations, no matter how serious, can be broken down to three questions you ask yourself or others ask you.

When it comes to preparing for retirement, there are so many differing rules, theories, planning tools – in my mind I need to consider retirement similar to a zombie apocalypse.

Sort of puts things in perspective, doesn’t it?

If today, you could clear all the noise, reduce retirement planning to what concerns you the most, what you need to do to protect yourself – What three questions would you ask?

As I work with individuals to formulate personalized retirement strategies, three questions emerge consistently. As a matter of fact, it’s rare when one of these queries doesn’t arise.

Once you strip out the confusion, target the basics.

Focus comes down to three main concerns.

Random Thoughts:

A confident retirement comes down to the money coming in to a household.

Cash flow is everything.

Question #1: How much spendable income may I have on a monthly basis post-tax to keep me, or me and my spouse comfortable for 20 years? Simply put, how much can I have?

Why 20 years?

Let’s face it. The odds of becoming a centenarian are as slim as the dead coming back to life. OK, not that slim but infrequent enough to understand that age 100 shouldn’t be a default setting for retirement plans.

Everyone I counsel is asked to complete the thorough, thought-provoking life-expectancy calculator exercise at www.livingto100.com. Eight out of ten outcomes come in between 80-85 years old. Women average longer life expectancies at 83-86 years old. Per calculator results, men rarely live past 84 years old.

Thought leader Dick Wagner and author of the new book “Financial Planning 3.0,” in a recent interview with the Journal of Financial Planning, stated “financial planning is very, very young as a profession. If you believe that 1969 was the first year for the profession, then we’re into our 47th year. That’s not very many years if you compare it to other authentic professions.”

So who are we as advisers to indiscriminately assume that retirees are going to live to 100? I’m not sure why I see this occur so often. Maybe it feels safe. Perhaps it’s CYA. Regardless, it’s inaccurate.

Candidly, even if the profession were a thousand years old, longevity analysis would remain a slim, educated guess at best. I am 100 percent certain however that establishing retirement income plans to conclude at age ‘unrealistic’ is an exercise in disappointment. People won’t adhere to goals, milestones they find impossible to achieve.

Please plan for reality. Not fiction. A reach to age 100 will most likely lead to unsuccessful plan outcomes. You won’t feel secure enough to retire or you’ll wait too long thus placing the quality of life in retirement, in jeopardy.

If you believe, based on family longevity and state of health, that there’s a great probability of living to 100, by all means, don’t ignore preparing for the possibility.

The topic is challenging and uncomfortable to discuss. It requires acknowledgement of our own humanity.

A seasoned adviser doesn’t overlook or dance around the topic of longevity. He or she should handle the conversation with grace and honesty. After all, we are all going to die (and hopefully not return to life like in The Walking Dead).

It’s something we all have in common. We don’t seem to like to think about it happening before age 100, especially when it comes to retirement planning.

In the same interview financial futurist Dick Wagner continues his thoughts on the financial planning profession:

“The mission and purpose of financial planning is to work with individuals and families and their personal relationships with money and the fearsome forces that it generates. There’s something about ‘fearsome forces’ – it’s terrifying. I mean, it’s a quintessential challenge of the 21st century: just try to survive with this money stuff. People do something that’s really hard, which is to anticipate their needs of the last 20-30 years of their lives. Now how do you do that? You have no idea what your health will be, you have no idea what your date of death is, you have no idea how long you can continue to earn a living.”

Financial planners deal with plenty of their own fearsome forces. One source of angst is to have straightforward, yet sensitive discussions; balance the thin line between a portfolio and human life because as Dick Warner lamented, there are plenty of unknowns.

Take it from me – we’re not fond of zombies in the planning process but they do exist.

Before you look to have a retirement plan completed, take it upon yourself to go through a life-expectancy calculator. Sit with the outcome for a while. Do the results make sense?

Once you’re at peace with the information, share it with your financial planner. Incorporate it into your analysis. You’ll both be in sync. You’ll tackle fearsome forces together. The synergy will lead to reasonable goals, follow up and fulfillment.

Question #2: Will Social Security be there for me?

The assumption that Social Security is a dying social program, regardless of the generation, runs pervasive. Don’t underestimate the importance of properly integrating Social Security into your retirement arsenal. For the majority of Americans, this is their sole income for life.

So, let’s clear up several misconceptions.

According to financial planning thought leader Michael Kitces in a recent voluminous Kitces Report on the topic, the Social Security system is often considered “going broke” by 2034. At that time it’s believed the Social Security trust fund will be exhausted.

Most planning clients have a difficulty believing the funds will last that long. Per the analysis, the majority of benefits will still be paid through tax revenues on workers paying payroll taxes at that time.

Social Security recipients usually receive Cost-Of-Living Adjustments each year. An added bonus to an income you cannot outlive is inflation protection. Unfortunately, COLA is not in the cards for 2016 (a rare occurrence), however overall, Social Security remains the best lifetime income deal available to the masses.

It’s best a retiree in good health plan to wait until at least full retirement age (66, or 67) or possibly later to apply for Social Security. By the time I’m consulted for formal retirement planning, many recipients have already applied for benefits early – at age 62, in fear of not being “grandfathered” into the system and losing future benefits.

Unfortunately, unless a household is cash-strapped or a recipient’s health is poor, there’s rarely a reason to apply for Social Security before full retirement age.

Starting early will have a lasting impact to monthly payouts. For example, a person with a full retirement age of 66 who started Social Security at age 62 would experience a permanent 25% annual reduction in benefits.

When I began my career in financial services during the great bull market of the 80s and 90s, the numbers worked out favorably for a Social Security recipient to apply for benefits early and invest the difference.

Since the year 2000, this strategy has been less effective. Over the last sixteen years I’ve witnessed improving life spans, people working longer and unattractive returns on investment assets, which has made Social Security a formidable hedge against longevity and adverse portfolio conditions.

In addition, Social Security has become a stealth, forced ‘savings’ program for a majority of households stressed to save for retirement in the face of rising college costs, financially caring for elderly parents and adult children, underwater mortgages and chronic underemployment.

For most recipients, waiting until age 70 to take advantage of an 8% delayed retirement credit is a smart strategy. In a majority of cases a retiree should seek to postpone Social Security, enjoy a permanent 8% bump in benefits, along with annual COLA (Cost-Of-Living-Adjustments).

Question #3: What should I be afraid of? I don’t really know.

This retirement game is unfamiliar territory. You’re outside the safe or familiar zone (which in The Walking Dead, is a dangerous place to be). Don’t be shy. Nothing is off limits. After all, this is a new experience. You’re not an expert (yet) at this next life phase.

Why not ask a tenured planner what you should fear? Better yet – ask friends and associates who have been retired – what did they find scary about this new world? What had they overlooked? What are the mistakes they’ve learned from? What were their greatest oversights?

There could be enemies hiding in plain sight (it’s tough to trust anyone in a world overrun by zombies), that may be overlooked because you’re too close to the situation.

Frequently I receive questions about fear in retirement. They usually have little to do with money. Ostensibly, information regarding Social Security, healthcare costs in retirement and other crucial topics, is widely available. A comprehensive retirement plan will cover all important financial concerns as well.

What’s difficult to find because a person needs to live it to learn it, is information on how emotionally challenging it is to navigate from the accumulation side of the household balance sheet to the distribution mindset – The new reality where a retiree must depend upon his or her assets to survive. Being outside the protective walls of a job or career is rarely discussed in financial planning circles.

From my experience, it takes at least a year for a retiree to gain comfort with a change in lifestyle, a satisfactory portfolio withdrawal rate, a new purpose for a life away from the office.

Never lose sight of the power of simple questions.

If they can keep the survivors of a zombie apocalypse alive.

Think about what they can do for you.