“Guns don’t make you strong, they make you hesitate and respect the value of human life.”

Lucas McCain

With a foundation in New York, now a life (or mid-life), in Texas, I’m sensitive to the frenzied disparate bombardment of opinions.

About everything.

On social media it’s North meets South, again.

Gun control, border walls, homegrown terrorists. Workplace violence.

Kim Kardashian.

Donald Trump.

Rhetoric, vitriol.

Electronic bullets.

People blown to bits in 140 characters or less.

Makes me realize.

People are shooting off their mouths indiscriminately.

The world needs The Rifleman more than ever.

Let’s return to September 1958, shall we?

Turn the clunky black dial flush to a rich, mahogany console. Fire up the RCA Victor, boys and girls.

TV tubes resonate a low hum. They sound like the wings of a thousand agitated bees until a black & white moving picture emerges. Out of nowhere from behind thick glass.

No matter how clear the picture, a perpetual cinematic room for a clearer clear exists. You toil endlessly with dual rabbit-ear antenna rods.

Feverishly you orchestrate two straw-thin antennas, stare at the screen. Stop. Work again. An awkward tango with thin aluminum arms. You’re expecting magic. Only you know when it’s found.

Battling rabbit ears is lost to the annals of American household pop culture. The endless search for medieval high-def is history. Dead.

Warmth seeps in on air waves. Vacuum tubes that resemble bulbous laboratory vials glow yellow. Heat rises. Conjures a musty, heady aroma from a warm brown felt grid stapled to the back of the set.

Cozy up to a screen of the thick glass. Watch your arm hair come alive, tingle to attention from static electricity.

You feel good all over.

And then.

Mom bellows from the kitchen because of course, she knows everything.

“Don’t sit too close, you’ll ruin your eyes!”

The Rifleman, a half-hour western drama, ran for five seasons: 1958-1963. Prime time on ABC.

Chuck Connors portrayed chisel-jawed Civil War veteran Lucas McCain. A widower raising a young son Mark McCain, alone. Building a life, a ranch, in the fictional town of North Fork.

I feel the ladies fading fast.

“I don’t like westerns.”

OK, The Rifleman is officially a western. You got me. However, life lessons roll larger than thunder arteries blistering the clouds in Oklahoma skies. The guns, bullets, dust, horses, and saloon brawls are set dressings for stories of challenge and perseverance. True grit.

Now, let’s get those ladies corralled into readin’.

A 6’6″ Lucas McCain holds a rigid stance against the searing heat of nature. Overworked boots. Heels in dry dirt. His broad shoulders glisten wet under the blistering New Mexico summer. The straight-line high blue gushes the same color as his eyes. Jaw clenched in determination, he removes his hat, the felt brim dark with sweat.

The salty sting in his eyes feels good. He’s alive. One with the land. His land.

Cotton is wet-heavy. A blast furnace against his skin.

Soaked with the fire of his toil.

He pauses to toss his shirt. Abruptly, it lands with a thick thud and soaks the parched earth underneath. A seldom breeze lands cool on his back. At 37, Lucas is fit, perhaps more so than a decade earlier.

His bare torso is lean. Working the earth, relishing the ‘sodbuster’ way of life has made him hard in body, sharper in mind. His farming a cleansing of where he came from, buried under black-pitch soil mixture of the present. Hopeful yet guarded for the future.

For him.

For Mark McCain. His boy.

Lucas reaches for a nearby bucket. Drinks deep from it. The sweet liquid from the ladle is lukewarm but invigorating. He carefully pours the precious liquid over his upper body. Drops embrace and crawl down his tired muscles.

The anterior of his right shoulder is tight but pliable. It had to do. Only a short time for a breather. There are more chores before sunset.

Lucas returns to his regimen. The thick spade handle grips small in large, callused hands. It comes alive. Ironically, his hands could kill yet it was easier to save a life. Grow it, too.

Whew, the ladies have returned.

Lucas McCain. A man of determination and wisdom formed by serving as Union lieutenant in the Civil War. Behind steeled eyes that witnessed the worst of the human condition, Lucas McCain became a master of placing himself in another’s veins. He knew when to strike and when, as a man of wisdom, back down.

Yea, there’s much one can learn from watching, no observing, The Rifleman.

Random Thoughts:

Shot #1: How much pain will it take to release the truth inside?

The emergence of your internal compass, a definition of truth as it breaks away from the fence lines of long roads traveled. How does this happen?

An uncompromising life philosophy.

What I call “Rifleman’s Awareness” is not born of happy or pretty.

It’s not of sunshine.

The source is internalized writhing maggots. Thick layers of spilled blood that attach to every cell. A tight-wedged coagulation of unhealed festering wounds that slither from unresolved torment under relentless pressure. A billion lifetimes in the making. The rot of past trials go back that far.

Sharp enemies of the past, the ones that carry and cut with rusted blades, never die. They continue to pierce until an injured limb goes numb and severed. At that point, you’ve won against fear and pain.

The opportunity has arrived for you to crush hideous demons into beautiful diamonds.

Nothing can hurt you. The higher plain is no longer fallowed grounds but an endless bounty.

You must learn to train these devils to do your bidding or allow their disease to stick to you. Consume who you are. Who you can be. Until you’re dead.

The Rifleman corralled and controlled internal torment. He could aim and fire the perfect dose of justice every time. His skills with a rifle were legendary. Known for miles. His words were delivered with similar velocity as bullets.

It’s safe to assume from binge watching what moves Lucas forward is life earned (and learned) – a bloody war, the loss of a spouse, a vigilance over his only child.

It can take years, decades (perhaps never) to develop a personal truth, an internal guide that motivates daily actions. The release of wisdom from a greater guide than self is an exhausting, ongoing process.

Beliefs that seed in the soul can break away to help you conquer the renegades in black hats. The gatekeepers. The enemies. When forced to protect everything you hold dear, those seeds will grow to mighty oaks.

Your personal rule book will be lived only after you’ve tamed the beast of fear. That mastery comes from confronting and melting the freeze that is born of it.

But first, you’re going to need to understand who makes the rules and why.

If you feel sick going into work every day, ostracized for disagreeing with your boss, shunned by co-workers, well then you sort of know already.

You’re walking the path of The Rifleman.

Recently, my friend and greatest teacher James Altucher wrote about personal rules on Facebook.

You see, he appears to be a nerd. However, he’s a self-aware rifleman (armed with pen and a waiter’s pad):

ARE YOU FOLLOWING THE RULES?

The government has rules.

Schools have rules.

Society has rules.

Parents and then family have rules.

Relationships have rules.

I tried to follow all the rules. I was a good boy.

Sometimes it’s hard to keep track. The rule book is too big.

And then I got the phone calls. Why didn’t you follow that rule?

I don’t know. It didn’t make me feel good.

Well, if the only thing that is important to you is feeling good you would just kill and steal and lie to people all the time.

Why would any of that make me feel good?

Well, what does make you feel good?

Talking to you on the phone makes me feel good.

Aside from that.

Walking outside and looking at people. Feeling the last remnants of sun on my cheek before the winter comes.

Being kind to someone when they least expect it. Surprise makes me feel good.

Knowing that every now and then I can still make my teenage children laugh.

I gave a talk a few months ago and I heard my youngest laugh. That is the best feeling I’ve ever had. She laughed right after I said something that felt like it was breaking the rules (I forget the statement: I was describing either lying or stealing or saying something about my mom).

Seeing the smile of a woman up close after a first kiss. That makes me feel good.

Being with friends who love me and I love. Anybody else…and I don’t feel so good. I feel sick.

Feeling like I’m improving at something I love. Because that grounds me and let’s me enjoy the company of others with the same passions.

Feeling like I need less than I thought I needed. Because needing less allows me to float into the sky without feeling scared, without feeling burdened to the ground.

Feeling always like I’m exploring.

Writing something really really awful. Because who gives a fuck.

Like this.

—-

So many times I hear from people who say: I have to follow the career (or marry the person), my parents want.

Or someone says: I have to go to college or nobody will give me a job.

Or someone tells me: you should be around these people. They can help you succeed. (But I don’t like them so what should I do?).

Or someone says: I want to have ten million dollars to relax. And own a big home so I can feel roots.

Or someone says: You have to vote in order to have your voice heard in society.

Or someone says: I feel stuck because I can’t quit my job because I have all of my family responsibilities.

I built a prison for myself also. It had triple locks. It had lots of guards. It had solitary confinement when I was bad. I didn’t much like my fellow prisoners but they were in here with me so I figured I would be with them.

I felt ashamed when I broke the rules of the prison. When I went broke. When I didn’t take the career I was supposed to.

When I didn’t return the calls or network with the right people or when I quit without warning the job I didn’t like or lost the homes I could no longer pay for.

Or when I was thrown out of school or when I didn’t pay the IRS or when I didn’t love enough the people I was supposed to love. Or the things I have done when I was so scared about money I thought I would go broke and die.

Or when I tried to live in a homeless shelter just to meet women or when I demanded love back from the women who didn’t love me or when I cried because I was scared that my life would disappear and nothing would be left behind.

This was solitary confinement. And it was lonely and I was afraid.

And one day I walked out.

And nobody ever saw me again.

That is some Lucas McCain kind of shit.

Lucas’ motives are consistently noble. No. Perfectly noble. Even when he’s left little choice but to use his modified Winchester Model 1892 to take out villains, he is delivering justice. His guide is a higher calling. A shiny key to living a life in the rough.

When you do a Lucas on who or what threatens you (and you will; rifle not required), be noble in your intentions. Standing for something you believe in is important to not only you, but to others.

Half-assed nobility is better than none.

I worked for (was enslaved by) Charles Schwab. Plainly speaking, my perception, my code, defines them as bad guys in white hats. Difficult to detect a rotted underbelly unless you’re homesteading within their bowels for a spell (cowboy lingo).

They hide behind edicts created by terrifying gatekeepers and spend hundreds of thousands of dollars on vigilante attorneys to intimidate and in many cases, destroy others. They’ll lie in cold-blood to slaughter the warm blooded.

They live to frame you for horse stealing or cattle rustlin’ and immediately call for your neck in a noose and a swing until you’re dead.

Underneath their so-called ‘code’ rolls an insidious dark residue of unethical dissonance. I know their employees work in fear. At least 100 of them have contacted me. They reach out from the shadows. Punch smartphone keys from hidden places. They ask me questions about how to break free. I’m happy to provide information.

It’s part of who I am. Help others. Don’t ask or seek anything in return.

I cut the wire fence. I spoke out. I did a Lucas McCain.They tried for years to wipe me out. High-noon style. I was willing to go broke exposing them. Ultimately, they were exposed for who they truly are. I’m still damaged. It’s fine. I learned. I won.

Oh, I forgot to mention: Every noble effort requires spilled blood. Your own or others. Not literally, silly. Well, perhaps, but let’s not go there. Could be money, an internal organ, a relationship.

Be prepared to lose something close or dear to you.

However I now live according to my own definitions. Rifleman-style.

Most likely, aggressively staking out villains is not for you. I don’t recommend it. Like The Rifleman, know when to take pressure off the trigger.

Those with personal codes think clear. Even under tremendous stress. They’re in control. Admittedly, I’ve made mistakes. Lucas rarely outed the rogues or took violent action unless those he loved or he, was in danger.

Recall what James wrote: Walk. Never be seen again. Fleeing from a cancerous environment can prevent well, cancer. Or worse. A long meaningless life within an unhealthy, suffocating environment.

“There’s dark corners in everybody’s lives. Sometimes it’s doesn’t pay to poke around in them.”

Lucas McCain

Like Lucas McCain did on several occasions, retreat from the gatekeepers. But walk with your front to them. Don’t take your steeled glance off them.

Don’t blink.

Never trust the fuckers.

Heed The Rifleman: Sometimes it pays to stay out of dark corners.

Be at peace. Take your ego out of it and understand you cannot change those who harm others even if they do it unintentionally. However, you have a choice. They can’t fathom a choice. In their minds, their worlds, there are no other roads.

Hey, you can move to another town (North Fork is coming along).

Perhaps you require more time, life experience, sorrow, regret, before you act. That’s OK, too.

Your time will come. No need to exhaust all your ammo right now. I’m not saying you won’t need to fire multiple shots. I’m saying it’s not required for every situation.

You’ll choose what’s right. Live to die. Or die to live. Codes don’t need to be complicated. Simple and powerful will get the chores done every time.

Go ahead: Get ready to fire your first shot. Tap into the diamond of your greatest powers. What are your personal beliefs? The ones the gatekeepers seduce you to believe cause grief for them and great obstacles for you.

The ones that scare the rule makers out of town.

“The rules tell me I can shoot. My own rules tell me that I hate gunfightin’ and will avoid it until I can’t.”

Lucas McCain.

Shot #2: Be Lucas McCain for only an hour a day. What you tell your brain, it will believe. It’s that simple. For an hour a day be – The Rifleman. Embrace his spirit of uncomfortable wisdom. Navigate a tough, admirable road you’ve been afraid to travel.

Like my friend Tanya. She’s battling a bully. She’s relentless to seek justice against a predator and helping other victims to speak up. The episode has affected her health. However, she’s steadfast and has a deep passion for justice.

The Rifleman lives in Tanya.

Like her, take one uncomfortable action that will draw you closer to understanding why you were put on the planet. One heroic act before you go.

Never be afraid to question your personal code. Lucas did. He was willing to listen when people he trusted advised him of a misconception. He kept an open mind. He was seasoned enough to adjust his thinking. Humble enough to apologize (and mean it).

People tell me The Rifleman isn’t real.

I call those renegades out at high-noon to face their bullshit.

Perhaps I’m immersed. Too deep in writing for television. Regardless, fiction and fact are cut from two sides of a blade. One man’s reality is another man’s fiction. Fiction and fact co-exist and shoot from the same barrel.

One hour a day to heed a higher calling, an enriched life.

Not much to ask.

See those eyes? Lucas McCain is watching (I advise against resistance).

Shot #3: Don’t let bad guys off the hook until (unless) they have proven change. Lucas’ history collided with his present, often. He knew he couldn’t escape (for long) the bad inflicted on people or the horrific marks others have left.

In many episodes, the karma coach rolls into town. Like a wagon wheel across the mid-section. Straight out of the Oklahoma territory.

Lucas’ dark place.

Ironically, the beasts entered North Fork frequently (drama folks, is good television). At times, he overreacted to their presence. He relived what they did to him. Like it was yesterday, he recalled their evil behavior.

Those who had proven redemption were forgiven. The others? Well, a dead-eye trigger finger took care of them. Lucas believed everyone could change, even the vilest of characters. If not, western justice was served.

You’ve lived long enough to be fooled by the bad guys. I bet they outnumber your good souls 2 to 1. Most of them can’t change. Too far gone. You can’t shoot them. I wouldn’t advise it.

Unless ‘The Purge’ becomes a thing, then go for it. I keep my ‘purge’ list fresh.

Hey, you never know.

Nah, you don’t need to resort to anything ugly. As a matter of fact, even under the intensity blasts of an August New Mexico sun, beauty will eventually appear out of the dirt for a patient sodbuster.

The strength in beauty bursts from heat. Cold is death.

Heat is life.

So don’t forgive the bad ones. Whatever you do. Don’t let them off the hook. Forgiveness just for the sake of it, for nothing, is death by ice. A soul in deep freeze. It signals you’ve given the bad ones a free pass. It’s you crawling belly down through the tundra, all the way cutting your gut open, dragging entrails.

Forgiving those who never seek redemption is a crime against your own heart.

Forgiveness foolishly exposes your hand, weakness. The seasoned poker players of North Fork would shoot you dead before you back away from the table. Embrace the anger. Let it take you. Allow it to scorch a personal path to victory.

The anger furnace will fuse your internal organs into barbed wire. Every cell grows sharp and deadly. You’ll become a master at detecting the presence of those who put your mental health at risk and seek to drain precious internal resources.

Because if you don’t learn, it’ll keep happening. Until the darkness saddles up alongside you and sticks to you forever like the spiny wings of Canadian thistle.

Back to our regularly scheduled program…

One early Saturday morning, Marshal Micah Torrance found out some disturbing news.

A woeful cloud recently rolled into town.

And he needed to think fast.

Or a friend’s life held in the balance.

Behind heavy-iron lattice of a lawman’s office office, Micah appears to require Lucas’ assistance with reinforcing a shelf to the deep interior of the middle jail cell.

For 62, the silver-haired lawman is surprisingly swift in gait. With Lucas holding the shelf against the wall, ready for the marshal to secure it, Micah makes his move.

Backwards exit.

On quiet footfalls. Steady. Micah clears the heavy cell door, shuts it quickly with a loud clank. Lucas at first believes his old friend is reciprocating a prank that embarrassed Micah the night before.

Far from it.

Micah was protecting Lucas from himself.

Reef Johnson was back.

Reef Johnson.

Once Lucas’ best friend.

Until.

He shot him in the back.

Until.

He left him to die.

Until.

He attempted to steal Lucas’ wife.

Ten years had gone by. For Lucas, it was a minute.

It was said that Lucas and Reef could pass for brothers back then.

A decade later, Lucas cared only about one thing.

To find this man. Track him. Destroy him.

No pass go. No collect $200. Just a death wish fulfilled.

Locked behind the cell door, the rage in Lucas’ eyes turned bars into molten steel.

“Micah, let me out of here. NOW!”

Tough lives roll the travails of revenge road.

Both parties lose a piece of themselves in the gravel. Their souls forever connected in a demon’s gambol. They spin and grind worn under the passage of time, or death.

Or confrontation.

From behind stark-black lines of shadows. Into dust-frizzed daylight that slivers through wooden slats of an old barn wall, a man emerges from a distant corner.

Tired of running.

As the enemy moves into half/dark half/light, Lucas full of anger, gun sharp and raised. He is a thick step closer to get a better look at the fire, his invidious focus.

As slit light slashes across Reef’s face you can’t stare. You can’t look away.

His hair matted, disheveled.

Deep lines across his cheeks, facial skin as sallow as worn leather.

“I’m here, Lucas. I can’t run any longer. Kill me! Get it over with!”

This man. What’s left of this man. A man who once resembled Lucas McCain, smooth of youth, clear of eye was nothing but a shell. He looked 77, not 37.

Lucas lowered his rifle. Revenge no longer held captive the ready grip on the trigger.

“Lucas! You can’t leave me like this! Please!”

As The Rifleman created distance between himself and that barn. That place where his anger ceased. The place he left in silence, yet heard the screams for miles…

He realized.

What he felt was pity.

The heave in Lucas’ chest was sorrow.

This wasn’t forgiveness. Release wasn’t forgiveness.

Never forgive those who shoot you in the back and leave you to die.

Time and the universe will take care of those villains in the proper manner.

In due time.

Sit back. Tend to your fields. Nurture the ground.

Be patient.

Shot #4: Forge strong financial boundaries around you and yours.

The financial landscape post-Great Recession is enemy territory.

Oklahoma badlands.

Your money isn’t safe.

There’s not enough barbed wire to protect the homestead.

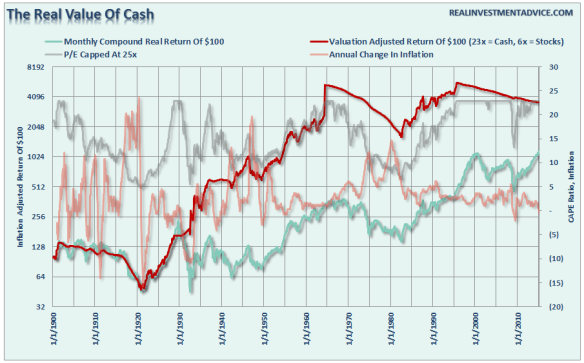

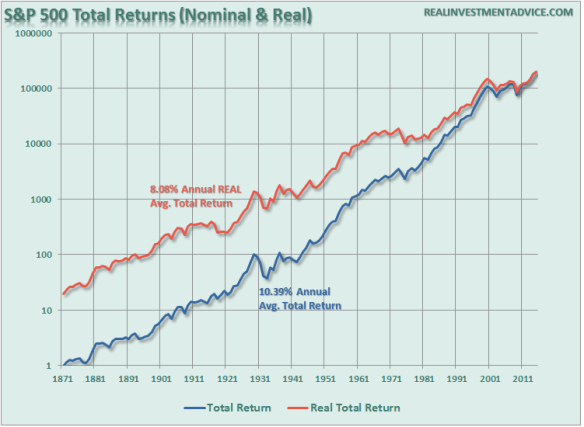

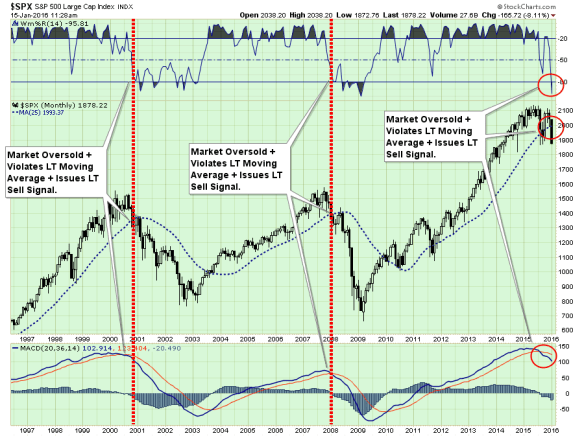

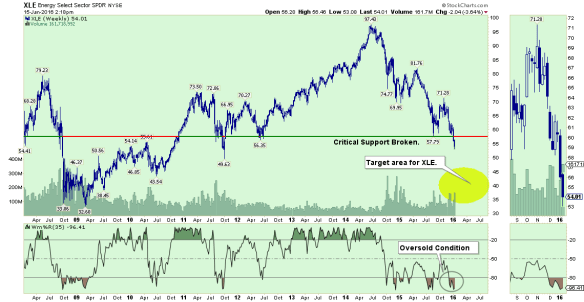

And the soil. Underneath the dirt, a bounty in stocks for 6 years or so, is over. Frankly, many retail investors didn’t participate in the 159% total return of the S&P 500 off the March 2009 bottom, anyway. They’re still trying to recover from the 2000 tech wreck and a flat-lined market from 2000-2013.

It’s still a whirlwind ribbon of dust.

Lance Roberts, Clarity Financial’s Chief Investment Strategist revealed his truth, discovered his rifleman years ago through his thorough, no-spin analysis of the stock market and the economy.

Refreshing. Rare.

The accounting magic used to prop up earnings, the foolish optimism of estimated earnings, profit-margin reversion. It’s all here, folks. You want fiery shots of wisdom in your gut? Read it.

And people call The Rifleman fiction and the stock market reality.

It’s silly, isn’t it?

Lucas is not amused by this information.

You shouldn’t be either.

Shot #5: Always teach and always expect nothing in return.

One of the greatest rewards in life is teaching others and expecting zero. It’s a positive rate of return to the world, the universe. It makes the stars shine brighter above a blue-black New Mexico sky.

The Rifleman shares memorable words, bits of shotgun-wisdom with his son Mark. He never holds back. Even when Mark doesn’t quite get it.

Doesn’t matter. Eventually Lucas’ invaluable guidance kicks in. On occasion, it saves Lucas’ hide.

“How can a man be so good with animals and so mean to people?

Lucas McCain: That’s a sign you’re growing up.

Mark McCain: What do you mean, Pa?

Lucas McCain: The older you get, the more questions there are without answers. ”

Today, I teach young investors how to not get killed by the buy-and-hold investment mantra and how true diversification includes investment in personal education and health.

I guide gifted financial services pros away from big box financial retailers and direct them to havens that have fiduciary intent. It’s a part of what I do. They’re my Mark McCains. My kids. I set them forth with noble intentions and a different world view.

How will you teach today? Who will you inspire?

Will you seek nothing in return except the stare at the stars in the sky?

Shot #6: now the difference between dumb fear and smart fear. Those who are reckless with your heart, your money, your emotions. Predators who dig beneath your vulnerability and then rip you apart from the inside, should be feared and avoided.

Individuals who have a track record of apathetic and non-empathetic behavior should never be allowed on the ranch. You’ll know them. You’ll be sickened by what you’re feeling. You’ll ignore what your intuition is telling you.

That’s plain dumb fear. And that will eventually leave you out in the desert with no water.

Vultures circling. Dead meat. You’ll crawl to safety but some part of you will be gone forever.

However, smart fear will keep you alive.

How do you develop smart fear?

Unfortunately, smart fear only comes with experience and knowledge.

You’ll require a construct. Questions are a solid foundation for said construct.

Create a simple framework to identify, fortify your defenses against enemies.

Start small. Big results.

All you need are three questions to get to the heart of anything.

My humble opinion.

Here’s a trio I use for dating (based on personal experience – yours will indeed, differ).

Let your inquiry flow naturally. You’ll become The Rifleman at separating friend from foe, now from forever, life from death.

How would you describe your long-term relationships with friends and family?

Big one. If she doesn’t have any close ties, or they’re full of weird sexual or resentful experiences I’m dodging a bullet.

Have you ever broken off an engagement?

Sure, nobody’s perfect: I’m just looking for an inability to commit, serial monogamy. Murder. “He fell from the upper deck on a Carnival cruise.”

How many times have you accused others of something you’re guilty of yourself?

Somewhat inflammatory. Granted. On purpose. We’re all guilty. I’m seeking to get a handle on frequency, accusations, assumptions. “Never” is not a good answer either.

Three questions.

For everything.

To create a personal SFDS – Smart Fear Detection System.

“It’s the price you pay on staying alive and in your right senses, it’s manhood. And I can promise that when you come to the far end of it, you’ll raise your old hands to bless this wonderful life you’ve been given, taken all together with the roast beef, and the moon rises, and a boy and his father riding out in the morning, after you’re grown up to be a father yourself.”

Remember – SMART FEAR SAVES A LIFE. YOURS.

Shot #7: Get in or cause trouble for the right reasons.

My favorite bullet. Hits me in the heart every time.

There’s a point in your life where you don’t give a shit any longer about what others think. You’ve been living your code. Those who fit in stay. Those who don’t, go. Life gets simpler. You begin to figure shit out, you begin to help others figure shit out.

The ranch is humming along, the crops are bountiful, the soil is the right composite, the enemies are at bay.

Then there are times when the trouble in your life resembles weather systems. When the turbulence begins, you also know it will pass. Makes it easier to deal with the aftermath, the cleanup. Healing.

And you can create your own weather. Spark your own thunder as the needs arise. For the right reasons.

Shot #8: Don’t be afraid to confront a person with their truth.

Lucas will place himself in precarious situations. Smack in the middle of the rough.Tip toe on the blade.

He’ll go out of his way to wake people up. Help them understand their truth. Most of us live in a state of denial. We hurt others, we lie, we make promises, we kill, we have little empathy and yet we want to be perceived as ‘good’ people.

Frankly, most people are assholes. They use you for what you can provide and then move on. That’s fine.

But make sure to tell them they’re assholes and deal with the consequences.

Perhaps you’ll enlighten. Regardless, you gave them some shit to chew on whether they like it or not.

Shoot the asshole a verbal bullet. Then walk.

You know how to eat shit, right?

Best not to nibble.

Bite, chew, swallow, repeat.

Because if you deliver, you’ll eat it, too.

Comes with the territory.

Shot #9: Learn when somebody confronts you with yours.

If you dare to shoot, you must be willing to be shot. You can’t protect yourself from a gunfight. The key is for bullets to graze, but not kill.

You must respect your opponent, however. That’s the key.

Hey, if you’re going to learn a tough lesson best to get it from a person you respect for whatever reason. Doesn’t need to be a grandiose reason. There’s just something about this individual you admire.

When Lucas shoots his mouth off and Micah gives it to him straight, Lucas doesn’t like it but he listens because he respects the marshal.

“Lucas, I think you’re wrong about this one.”

If someone provides constructive criticism, it’s acceptable, normal, to hate it at first. It’s fine to feel the sting of the words like bullets, and bleed out.

Right there on Main Street, North Fork.

Just as long as you step back, dig out the fragment. Feel the pain. Examine it. Ponder why you were shot. Was it one of the best shots of your life?

Learn from the bullets that hit and take you off balance.

Just as long as you respect the shooter.

Otherwise it’s an enemy and you need to return the blast.

Rifleman-style.

Shot #10: Stick your neck out for those you love. Place your neck in the noose if it means someone you love remains happy, moves on, sticks around.

What else you got?

Sacrificing a part of yourself for someone you cherish isn’t a bad thing. It’s walking like McCain.

I did it for clients and a fiduciary right to care for them.

You’ve done it for children. Parents. Friends. Animals.

Recognize, remember, reward yourself for sticking your neck out for those you love.

Heck, you’ll be called horrible things. I know.

You think everybody loved Lucas?

Why do you really think he needed that rifle?

The thing in this life is to stay alive. Ride easy.

Like in the old west.

Lucas McCain never spoke the words at the start of this blog post.

As I write dialogue for television I place words in mouths of fictional characters. The commentary would have been delivered perfectly however. I can hear the deep-baritone voice of The Rifleman resonating right now.

You don’t get endless shots at this stuff because eventually you’re in adult diapers and drooling into a liquefied breakfast.

Give yourself a number. I chose four.

Four bullets in my rifle.

I believe Lucas suffered from overwhelming, lasting grief that he channeled into something bigger than himself.

Last, I learned from Lucas that death isn’t frightening.

Bad memories?

Ghosts from the past?

Now they’re frightening.

They haunt, relentlessly.

Yet there’s something good that arises.

When the demons dance.

They create.

Riflemen.

Dedicated to radio host, veteran broadcaster, all-around good guy and most important: Hard-core “The Rifleman” fan – Gary McNamara.

Special mention to dear friend Tanya Bilisoly, Austin realtor extraordinaire who is taking on a bully, living her “Rifleman moment,” right now.

They’re comin’, they’re comin’!

They’re comin’, they’re comin’!