I appreciate rules.

Rules derived from the heart and mind have saved me.

Rules, forged from experience, can safeguard precious resources – financial and otherwise.

They will protect you from losing your pants.

Naked rules are best.

Pure, simple, raw.

Here are mine.

What are yours?

Random Thoughts:

Part I: Life Rules.

If a woman can’t listen to the Eagles’song Lyin’ Eyes without wincing, or quickly changes the station, run.

Beware of people who carry a stash of ’emergency’ condoms (indeed run, but feel free to have sex first).

You can’t wipe your ass enough (especially men – we’re the worst). When you believe it’s all clear in the deep, take another swipe. Just to be safe.

Never trust a person who rarely uses turn signals.

Be cautious of those who judge based on past mistakes when they’ve made the same ones or worse.

Don’t step back without looking (there’s a dog there, especially in the kitchen).

Never let open wine go to waste. Never. (Did I say never?).

Distrustful people are black pitch through the soul. Avoid them.

Be wary of those who can’t maintain close long-term relationships of any kind.

When I ignore rules I create, bad things happen.

Misjudgments remain with me. I see injury in the mirror every day. I lose a spark that will most likely, never return. Perhaps it’s part of a natural process, like aging.

Living without a personal guide book can hurt you.

Along with Clarity’s Chief Market Strategist Lance Roberts, we’ve created rules to help you protect and understand the key drivers of your wealth.

Remember – For every beginning there is an end. Investments have a shelf life. Eventually you’ll need to liquidate them to fulfill a financial goal, create a paycheck in retirement, gift to loved ones. Whatever. Money is to be spent, enjoyed.

Not hoarded.

And yes, you can indeed sell investments to protect capital.

Huh? What?

Sell: The scariest 4-letter word on Wall Street. Just the mention of it and you’re branded a loon. Leprotic, running amok and licking the neighborhood children.

Part II: Investment Rules:

Cut losers short. Let winners run. Underperforming positions are reduced or removed from portfolios on rallies.

Set financial life benchmarks and take action. Every position purchased has a sell target. Investments without goals are arbitrary, which increases portfolio risk.

Emotional biases are not part of the investment management process.

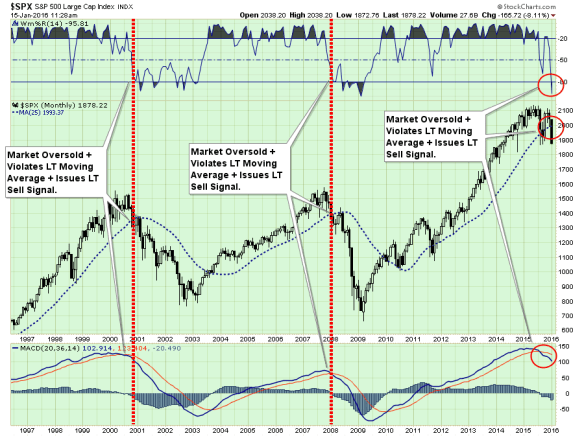

Follow the trend. 80% of portfolio performance is determined by the underlying trend.

And the current trend is south.

When markets break their long-term bullish trend supports combined with important long-term sell signals and a sharp decline in momentum, it has historically denoted the start of a “bear market trend.” The red highlight denotes the start of the bear market. The yellow highlight shows the ensuing bear market completion.

Never let a profit turn into a “loss.”

Investment discipline is successful if consistently followed.

Losses are part of the investment process. Losing positions are regularly culled to reduce portfolio risk and free up capital for better investment selections. However, you can’t completely avoid losses. Sorry. If that’s the case you’re better off in certificates of deposit. You can minimize but not eliminate. You play, you pay.

As fiduciaries of OTHER PEOPLE’S money, the biggest concern is not how much money we make during market advances, but rather how much we keep from losing during market declines.

While this seems counter-intuitive, in reality it is where long-term gains are generated. As William Lippman, CEO of Investment Management at Franklin Templeton quipped:

“Better to preserve capital on the downside rather than outperform on the upside”

A strict discipline of portfolio risk management will NOT eliminate all losses in portfolios. However, it will minimize the capital destruction to a level that can be dealt with logically, rather than emotionally.

This isn’t market timing, people. That doesn’t work. ‘All-or-none’ is a losing strategy. Never go all cash. From a management standpoint, this is a bad idea. Trying to “time the market” is impossible over the long-term and leads to very poor emotionally based decision making.

The objective is to reduce portfolio risk to manageable levels to preserve capital over time. We can do that by increasing and reducing our exposure to equity-related risk by paying attention to the price trends of the market.Odds of success greatly improve when the fundamentals are confirmed by the technical indicators (see? Another rule).

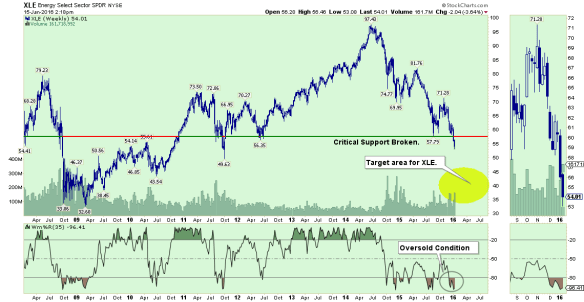

Don’t add to a losing position. This is called “averaging down” and rarely is it effective. How many investors are caught in the energy sector value trap? Or treated master limited partnerships ‘safe’ as fixed instruments?

The slide has been ugly and getting uglier.

Don’t be a hero. Buying energy or “averaging down” at this juncture will most likely be hazardous to your wealth.

Markets are “bullish” or “bearish.” Remain neutral or long in bull markets. In bear markets be neutral and increase cash.

When markets or portfolio positions are trading at extreme deviations from long term trends, do the opposite of “the herd.”

If you haven’t trimmed positions yet –Wait for an opportune time. Most likely, a market bounce is coming. Trim your weakest holdings into strength especially if your gut is in turmoil or you’re 5 years or closer to retirement.

A goal of portfolio management is to achieve a 70% success rate. No process is perfect. Consistency wins the long game.

Manage risk and volatility, not returns. Also, manage emotions. Humans are not wired to invest. Knee-jerk reactions, overconfidence, seeing trends that don’t exist will only destroy portfolio returns.

Never discount the importance of financial planning. The investment process is an element of a financial plan. An important one. However, it’s not the full story. It’s the sexiest chapter, I know.

There’s more to consider.

So we created.

Part III: Clarity’s Financial Planning Rules.

Take a holistic approach. Proper planning integrates all assets, liabilities and sources of income for a complete perspective.

Money is fungible. For planning to be effective, remove the mental boundaries around the dollars you earn and save so they may be allocated to their highest and best use.

Don’t discount Social Security strategies. Take steps to maximize earned benefits. Coordinate Social Security withdrawals with those of other accounts to minimize the impact of taxes.

Healthcare costs including Medicare, and senior housing options must be included in the planning process.

Successful plans are grounded in financial self-awareness which includes prioritizing needs and wants.

Conversations with loved ones and friends about aspects of your financial plan are important. Make sure your estate, gifting and future housing intentions are clearly communicated.

Don’t Get Fooled By Averages. The financial markets do not return 8% a year. A realistic financial plan includes variability in returns, including losses, over time.

Accountability Matters. A financial plan not followed is not a financial plan at all. Long term financial goals need to be broken down into monthly objectives and you and your adviser are accountable in meeting those objectives. (It is easier to consider a savings goal of $500/month versus $6000/yr.) Mental trickery works. Milestones broken down to millstones will convince your brain to take action. Move forward.

Rules.

Boundaries.

They work.

Follow them.

Survive.

With less wear on your face.

Less dark circles under the eyes.

You’ll preserve joy in your heart.

Stamina.

Will be yours.

And you’ll live to play another day.

For a glossy (fancy) copy of our investment and planning rules email me at RichardRosso@myclarityfinancial.com.

Charts by Lance Roberts. Sign up for his weekly market/economic newsletter at http://www.realinvestmentadvice.com.