Media is flooded with pundits spouting 2014 financial resolutions. Heck, I’m on radio and television talking up the same.

Increase savings in retirement accounts, pay down credit card debt, check your insurance coverage for gaps – all good advice.

But.

We already know this stuff. It’s drilled into our heads.

Every year.

It’s fine to be reminded of the healthy financial actions we should take.

Yet, what stops us from following through?

Before you ponder money improvements for 2014, think outside the box – deviate from the worn financial paths you have attempted to walk before.

This time you’ll succeed if you take five different paths.

1). Don’t save everything for retirement. You read it right. It’s been drummed into you how a secure financial future depends on maximizing contributions to tax-deferred options like 401(k) accounts. But how important is it, really?

A.J Leon, writer, motivator, world explorer, big thinker, in his book, “The Life and Times of A Remarkable Misfit,” outlines 16 simple steps to make money and lose respect – Step 4 is: “Never invest in yourself. Instead sock every last penny in a 401(k) that may or may not be there to greet you when you turn 65.”

Many employers have a difficult time understanding retirement plans. From the hundreds of plans examined, I notice an overwhelming trend of bland choices coupled with high fees.

For some it’s best to settle on government-approved choices called “target-date” funds. They’re the prevalent cookie-cutter choices in your company retirement plan. Basically, they’re an all-in-one mix of mutual funds packaged and wrapped in another mutual fund, thus called a “fund of funds.” The mix of stocks, bonds and cash is designed to match up to the year you decide to retire.

For example, it’s 2012 and you’re 40 years old. You are planning to retire at 65 (good luck). You decide on the “BlahBlah Fund 2037.” Easy.

The logic behind a target date fund is simple even though underneath, the design is complicated and investment philosophies can deviate dramatically depending on the mutual fund family your employer utilizes. In other words, the returns of the Blah-Blah Fund 2037 compared to the returns of your buddy’s La-La Fund 2037 will most likely differ, sometimes radically.

Let me clarify: Each fund creates a “glide path,” which means the blend of investments should gradually become less aggressive the closer one gets to retirement or the target year.

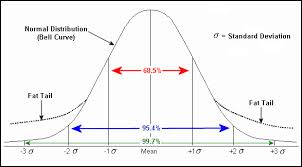

Per research by Zvi Bodie, the Norman and Adele Barron Professor of Management and Jonathan Truessard, Lecturer, both at Boston University in a 2007 paper “Making Investment Choices as Simple as Possible: An Analysis of Target Date Retirement Funds,” target date funds are approximately following the well-known rule of “100 minus your age,” for the stock portion of the mix. And this smelly piece of financial dogma needs to be abolished. Now.

Target-date funds require refinement. For those who invested their tax-deferred dollars in 2008 target-date options, hoping to begin withdrawing the money in 2008, were in for a rude awakening when their accounts suffered by over 21%.

Consult an objective financial advisor; select a balanced fund. If your choices are limited to the target-date variety, cut the “maturity” date in half. Your estimated retirement date is 2020. That’s six years away. Go for fund 2017. Be prepared for a 2008 surprise.

Contribute up to the employer match. Don’t leave free money on the table regardless of choices, either.

According to Federal Reserve data, the average U.S. household maintains an outstanding credit card balance of over $7,000. Based on numbers provided by www.bankrate.com, the average annual percentage rate or APR for variable-rate credit cards stands at 15.37%; fixed-rate cards stand at 13.02%.

Maybe, just maybe, your 401(k) account returns exceeded 13-15% in 2013 so it was worth carrying a credit card balance. Long term, it’s a bad financial choice. Instead of maxing out saving for retirement right now direct financial resources to pay credit card debt off in full.

2). Consider your human capital. Quantify your worth. You are your greatest investment. I know it’s tough to think this way, to choose yourself, but it’s true. Return on self-investment is wealth yet to be achieved.

How will you increase your value in a challenging marketplace? Perhaps it’s a new skill necessary to move ahead and above a nascent U.S. economic recovery.

If a continuing education opportunity exists or improvement options are available to increase your income, do it. You’re probably never going to retire anyway and when you do decide, it’ll be much later than age 65 so maximize the ROY (return on you) today.

Check out a Human Capital Calculator here.

3). Get your head straight. My friend Shanna and I discussed this topic, recently. If you are jealous of those who have prospered financially and you communicate negative sentiment to others, you’re digging a toxic mindset hole that will be tough to escape.

Don’t talk yourself out of empowering money habits. It’s the lazy way out. Jealousy is an energy sucker, a cash drainer. Change your mind set in 2014. Your brain will believe what you repeat to yourself, to others. Ask more questions of those you “envy:” How did you meet your goals? What are the daily habits you follow to gain greater financial independence? What did you learn from your mistakes? Learn from others, don’t push them away.

Teacher, mentor, investor, best-selling author James Altucher advises:

“You have a house. You need to keep the house clean so the right guests can arrive and feel comfortable. If you clutter it with anger or envy or scarcity or fear then abundance won’t feel comfortable moving in. I say this not from a position of comfort but because when i was dead and buried, i had to clean the clutter to make my life work. And it was hard because when the house is cluttered, your mind gets depressed and lazy.”

4). Stocks are not an end-all investment. Don’t be pushed into believing stocks are the panacea the financial industry tells you they are when it comes to fighting inflation. According to Jim Otar, creator of the Retirement Optimizer and author of several books on retirement planning expanded on this topic for a recent interview:

“Many advisors are under the assumption that stocks always beat inflation. This is not true. Equities beat inflation only during the long-term bullish trends, which occupied 43% of the last century. During the remaining 57% of the time, equities did not beat inflation.”

Rental properties, oil & gas interests, angel investing (can be RISKY), inflation-linked securities, deferred-income annuities can also battle inflation and diversify a stock portfolio.

5). Stop the competition. I hear it often: My friends are the same age and they have: More cars, more savings, more stuff.

Stop.

First, friends embellish.

It’s called the endowment effect.

Second, your best financial life begins today.

Don’t look back.

It’s never too late.

Third, forget the stuff.

Travel lighter.

Down five alternate paths.

And discover long-lasting financial success.