Once upon a time, (allegedly), there was a dude named Moses who delivered chosen people from a horrific situation. Important man. Very Popular. Scruffy. Like Rick Grimes (Google if you must).

Beards are in, people.

Then there was God, a prolific writer with his finger (imagine) who decides (who’s gonna argue?) that Moses was to be the recipient of two stone tablets which pretty much outlined the Big Guy’s marching orders for humanity. I’m talking serious stuff.

I wonder what happened to those historic slabs.

I imagine them as Carl Icahn’s cocktail coasters or used to gain traction in snow wedged underneath the rear wheels of Mark Cuban’s Land Rover. Many heroic things die cowardly deaths. Keeps me grounded to think that way. I know. Sad.

Anyway.

The words, the commandments, ten of them, were as heavy as the rock parchment they were carved into.

Three out of the Ten Commandments focus on “coveting.” Wives, animals, houses, servants. Coveting is definitely a big no-no.What’s coveting?

According to Merriam-Webster it’s a verb. It means:

To want (something that you do not have) very much.

Oh you were able to take a decent stab at the definition. You did good.

You’ll see where I’m going here, be patient. Jesus, our attention spans are down to the time of the sex life of a tsetse fly (they mate once and then I think they die). Thanks internet!

What I’ve learned after 27 years serving clients, 14 of them at the “client-first” (more on that later,) branded financial-services behemoth Charles Schwab & Co, is that this marketing and legal locomotive that blows money like engine steam, aggressively seeks to barrel over everything it touches. Once they’re done, you may as well be as flat as a nickel on heated rails.

Actually, covet is too polite. Way too generous.

To be clear: Once the Schwab Kraken is released on anything or anyone, the beast attacks, grabs and seeks to destroy its prey. You are property, lock stock and barrel of the Schwab brand. Your former identity is a cold shadow of the past. Whatever was once noble, honorable, fiduciary, ostensibly is digested by the venerable appetite of frenzied shareholders.

Whatever remains of the target is regurgitated; never to resemble its original form.

For example, who’s the brilliant guy who ran Windhaven, a separately managed account, after Schwab purchased the company he founded? I can’t even find him in cyberspace.

According to a WSJ article:

“Mr. Cucchiaro left Windhaven “for personal reasons,” according to a news release issued Friday by Schwab. A spokesman for Schwab said there was “no relationship” between Windhaven’s recent performance and Mr. Cucchiaro’s departure.”

Hey I know. He changed his identity and is now living on a remote island replete with pina coladas and coconuts; or perhaps he was cast away and a soccer ball named Chuck is his cherubic best friend.

All I’m saying is once you’re swallowed and spit out by the Schwab soul sucker, you’re sort of different. Perhaps you’re missing a part of yourself. Oh hell, maybe you’re just missing (literally).

God speed, Mr. Windhaven.

Heck even the dead aren’t safe from the clutches of the corporate creature.

From what I learned firsthand (no kidding), as a client you’re worth more dead than alive. Your mortal coil may have shuffled, but at Schwab, that coil remains as warm as a newborn baby’s head during a ten-hour breech birth.

Your beloved assets shall be entombed in an eight-digit account number fortress. Money interred. Not only that, surprisingly, your heirs will deposit even more of your money at Schwab, after the last of the flowers wither on your grave and dead leaves wind blow into a pile at the foot of dear Aunt Millie’s gravestone.

I don’t know about you, but that makes me fuzzy all over. Such a caring organization. Can you feel Uncle Chuck’s death grip embrace your eternal liquid net worth? My cockles are warm. Cockles.

Are yours?

So, why should you care? Why does it matter that two financial services companies are having a very public fight over a product and sort of punching below the belt?

For me it sort of feels like the first time I watched “Godzilla vs. Mothra.” I mean I love this stuff. Pass the popcorn.

If you use financial services of any kind, there are very important messages for you here. Pay attention because as an investor you’re a winner; you’ll be a winner. Competition will benefit you.

And Adam Nash, CEO of WealthFront like Davy Crockett at the Alamo, is willing to fight.

First, Mr Nash, this isn’t Charles Schwab. It’s Charles Schwab & Co. They are not the same. I’m sorry. I learned the hard way. I paid with a kidney and half a million bucks. Throw in a family, too while you’re at it.

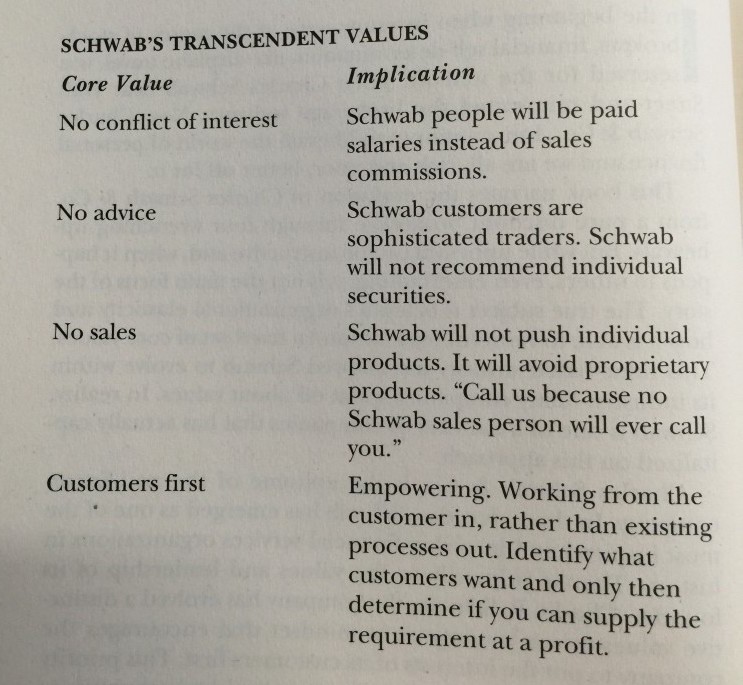

It’s shareholders and a CEO (Walt Bettinger) who is turning (turned) a brand into something so far from Chuck’s values and visions, that when I asked various management types in 2012, what exactly is the company’s values and visions? I could not get an answer. Zero.

You see, that above (good book from Mr. John Kador), is fantasy land now. That was 2005. Might as well be 1805.

Ancient history.

It’s Strawberry Shortcake starring in Fast & The Furious 8. Not going to happen. And you see that customer first verbiage? It’s shareholder first. Regional management told me that. Shareholders first, THEN customers. I was told.

To my face.

So you know what Mr. Nash, you win. And so do Schwab clients and other retail investors who read your words. I could feel your disheartened spirit, your awakening, your suspicion. Although I could argue specifics about fundamental indexes, in all fairness to the Schwab Robo, I find benefits to the strategy over WealthFront’s.

BUT THAT DOESN’T MATTER.

What matters is you have a vision I wasn’t aware of. I was wrong about WealthFront’s motives. What matters is you ripped a hole to expose the hypocrisy (client first on the surface, a bitch to margins, underneath), that has permeated and changed permanently the Schwab culture. And now people will know. And that’s worth something in a world post-financial crisis, which seems to be owned more than ever by financial services and central banks. Broken values and bottom lines sum up the financial sector since 2010, in my opinion.

You have a passionate mission. Unfortunately, you’ll sell out. We all do. But we can come back. We all get a chance to come back. I did. Perhaps Mr N you will have a chance, too.

Mr. Nash? I have confidence in you.

I have more confidence that you would come back because the Kraken can’t. You can’t turn the heart of the beast into Hello Kitty no matter how idealistic you seem to be in your writing.

Oh, and I really like the beard. Did you shave it? Grow it back. Because like Rick Grimes in The Walking Dead, you are now at war.

And a beard works on you.

I hope you win. I did.

Here’s Mr. Nash’s first attack.

Copy and paste (darn you, WordPress).

View at Medium.com

Bottom Line: The brokerage gods gave Chuck (Moses) the insights on how to treat clients and employees – the 10 commandments (which he wrote,) and then Moses shattered them and decided that coveting was OK, especially if it benefits your stock price.

Random Thoughts (for investors):

I’m not sure of this whole roboadvisor thing. It was created out of the failure of all of us in the business to do what we said we would do: Tax harvest, rebalance portfolios, be objective, provide low-cost options, and to examine a client’s financial picture. holistically before making recommendations.

I got in trouble for that at Schwab. I was there to SELL product, not help clients reach dreams. I was a Certified Financial Planner who worked at Enterprise Rent-A-Car. Which fee-based car can I get you in? Then wave goodbye.

Frankly, fuck Walt Bettinger’s dreams, I could care less. I hope he gets cast off to an island like Mr. Windhaven. Chuck needs to take his company back (again) and align with clients and employees. Only he can kill the Kraken. Wasn’t that Liam Neeson in Clash Of The Titans?

Ohhhh, that’s what this is between Robos – Clash of the titans.

I also do not believe in efficient markets which is how all robos operate. In other words, there’s no such things as asset bubbles in this arena. Well, let’s consult an expert, professor Bob Shiller from his latest edition of Irrational Exuberance.

“The point I made in 1981 was that stock prices appear to be too volatile to be considered in accord with efficient markets. Assuming that stock prices are supposed to be an optimal predictor of the dividend present value, then they should not jump around erratically if the true fundamental value is growing along a smooth trend.”

More.

“Fluctuations in stock prices, if they are interpretable in terms of the efficient markets theory, must instead be due to new information about the longer-run outlook for real dividends. Yet in the entire history of the U.S. stock market, we have never seen such longer-run fluctuations, since dividends have closely followed a steady growth path.”

Still more.

“There is a troublesome split between efficient markets enthusiasts (who believe that market prices accurately incorporate all public information, and so doubt that bubbles even exist) and those who believe in behavioral finance (who tend to believe that bubbles and other such contradictions to efficient markets can be understood only with reference to other social sciences, such as psychology).”

And investors were sold the story, are buying in strong to the story again, that stocks always outperform other investments.

More again from the professor (last one I promise, I’m a big fan):

“The public is said to have learned that stocks must always outperform other investments, such as bonds, over the long run, and so long-run investors will always do better in stocks. We have seen evidence that people do largely think this. But again they have gotten their facts wrong. Stocks have not always outperformed other investments over decades-longs intervals, and there is certainly no reason to think they must in the future.”

You gettin’ it, yet?

You’ve been sold a bill of goods to set a portfolio, always remain invested and don’t worry about the real earnings or valuation of the markets at the time you commit capital.

You see it’s easier for the financial services industry, whether it’s through the front door like WealthFront or backdoor like Schwab, when it comes to a robo, if you buy into it, to capture your assets during a bull market. And low cost is BIG volume.

And of course, it’s all long term. Long-term is a fuzzy blanket compliance departments love.

Sell is a dirty, four-letter word. Sell my stocks? Protect my capital? We can’t do that.

Did you forget about asset bubbles? Your portfolio hasn’t. I bet it hasn’t recovered from the 2000 Tech bubble, yet let alone the devastation from the financial crisis. And as an ultimate kick in the groin, your house went down the toilet, too.

Nope. I’m not buy and hold for me or clients. I never will be. I have sell rules because the math of loss is more devastating than the wealth from gains. But I tell you this, if I did invest that way, I’d give my money to Adam Nash because his heart is in the right place.

Yea so, I like some of the research that went into the Schwab product but you seem less like cattle with WealthFront and more the butcher. And you never want to be the cattle.

At Schwab, whether you’re an employee or client, you are expendable and a number. OK, I’m not saying WealthFront is altruistic (although after examining their numbers I still don’t get how they make money for themselves) but at least there’s a vision for Christ’s sake.

At Schwab, you’re cattle to milk the bottom line. Even after you’re dead. I’m certain of it.

Whether you invest with one or not, find a fiduciary to consult at least on an hourly basis. A fiduciary is there to help you make big, holistic life and money decisions and assist with your portfolio allocation in an objective manner. The financial services industry doesn’t want employees to be fiduciaries, to place client interests first.

It’s fine we make “suitable” recommendations, but to me that means what makes the most for the firm and ourselves. Suitability is there to protect the firm. Not you, the client. It’s to make sure that company asses are covered and boxes checked in case you get ticked off and seek to take civil action. Tax bracket, got it. I’m covered. Sell you a product, move on.

I had to pay half a million bucks to be told by a Schwab-hired attorney that “Richard Rosso, you are not a fiduciary.” No shit.

Now I am. I acted as such then and would do it again.

I’m interested to see how this battle turns out.

I’m on the side of investors, and now, Adam Nash.

I hope he prevails.

Maybe I just have a bone to pick with a large company that sought to destroy my life.

Could be.

I can’t rule it out.

All I know is we need more thought leaders like Adam to provide candid, heartfelt communication.

It’s long overdue.

And it makes me happy.

You should be too.