I was (am) a huge fan of the iconic Planet of the Apes movie franchise.

The original films: Not the attempts at remakes.

Shameful.

“

“

You blew it all to hell – I blame financial services.”

Every six months, in the early 70s, there was a Saturday “Go Ape” marathon at the Brooklyn neighborhood movie theatre (the Mayfair), which provided parents a rare opportunity to unload the kids for an early morning into late afternoon.

God knows how many children were conceived during an Ape-A-Thon weekend. We would sit all day (or try) and watch all five POTA movies in the original order they were released to theatres – Beyond the apes, revenge of the apes, beneath the apes. Ushers dressed as apes. It was magical.

The Sunday after Ape Day was a time of rest and repulsion for anything hairy (I didn’t even want to pet the dog).

Confusion set in for me after the third installment of the simian series (Escape from the Planet of the Apes). To this day, I’m still puzzled.

Movies with any hint of time travel remain a frustration.

After watching (and taking notes like an asshole) the film “Inception” six times I still don’t understand what the hell happened at the end. My mind, the ability to think, falls into a black hole if I’m required to follow a story line through space, time, dreams.

I work to follow the sequence but I tune out in a huff.

Lord forgive me. I’m just not that smart.

Let me try this again.

The ape planet turned out to be Earth (shocker!). Got it. Andddd the astronaut (Taylor, played by Charlton Heston) who landed on said ape planet eventually blows it (Earth) literally to pieces by triggering a massive nuke. Worked through that ok. After that? It’s a time forward/backward hot mess.

The first talking ape (Ceasar) born on Earth alters the course of history in 1991, I think. Planet of the Apes begins! Ceasar’s mom Zira after getting loaded up on too much “grape juice plus” aka champagne slurs out that Earth blows up in the year hmmm 3950. That’s how she says it: “Hmmm, 3950.” Like a drunk monkey.

Zira tipsy on “Grape Juice Plus.”

SO the parents of the ape who began a simian revolution in 1991 saw Earth blow up in 3950 and the astronaut who landed there in 1970 was responsible. You see where I’m going with this? I should think it through but I’m just not patient or perhaps, smart enough. Frankly, I don’t desire to be this clever.

Confusing yes, yet still more logical than the financial industry’s holiest grail:

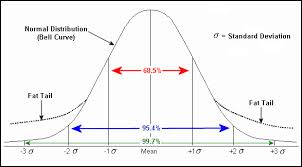

The dreaded “normal” bell curve.

The sinister creation that almost ended my career, my professional life.

I’m habitually a big fan of anything curvy, but this one is deadly. A dead man’s curve – obviously my mental train of thought derailed early on believing in this myth.

I was brainwashed to believe in this curve from the very beginning of my career.

I trusted my teachers.

Why the hell not?

The curve is so logical, clean, warm, comfy, rational, explainable and seductive to us investment types. It’s easy to sell to the masses. It makes brokerage firm compliance departments happy.

The curve provides financial services firms who churn out assembly-line advice, an academic free pass. Empirical justification to ignore the research which followed, proved how the curve was a mathematical convenience, not realism (Mandelbrot & Taleb inspired words of beauty, not mine).

I asked my former employer and others to remind me why we believe in this damn thing.

No answer.

I experienced a flashback: I was back in high school and the popular girls were ignoring me again.

“You get a load of Rosso’s man boobs? And he’s only 15!”

Back to the curve:

It’s a mathematical Snuggie of sorts.

It frees hours to sell financial product – Set the money and forget it because stock price movements are random anyway. Don’t stress out. There’s a study out there that proves I can sell you an homogenized portfolio solution and move on. I have sales goals!

The curve provides a sense of accomplishment, finality to a risk management process that has no end. Frankly, during one of the greatest stock market bull cycles in history (which is gone 13 years now), it worked.

The Gaussian curve when applied to portfolio construction or risk management, underestimates risk. It applies an “everything is gonna be alright,” attitude to every stock market cycle as if every one is a secular (long-term) bull market.

The curve disregards the big moves that wipe you out financially. Huge moves that deviate from the average are well, ignored.

Heck, when you think about it, the curve does describe investors and markets perfectly, right?

Humans are so rational and logical. I guess curves which apply to them should be too?

The curve fooled, “assured me” the failure of Long Term Capital Management was an event that should have occurred every 4,000 years. Unfortunately, I wasn’t reading enough Mandelbrot, Minsky, Taleb or Otar.

No problem. Next disaster I’d be long, long gone.

Easy enough.

Then.

The tech wreck happened.

Still believed. Was told again by my former employer, to believe.

“Yep, I was Natalie Wood. The curve was my Santa gone bad. Bad Santa!”

Then the financial/housing/banking crisis kicked us in the groin five years ago. I think of Hans Moleman from The Simpsons getting his noids smashed by a football.

But this time I wasn’t going to be fooled.

No more Hans Moleman. On the ground. In the fetal position.

Nope.

Oh..

Here’s how some of my questioning to those smarter than me at my old firm went in 2007 when sub-prime issues were gnawing at me. I asked the same questions in 2010. Amazingly, I received identical responses.

Both times I asked.

“Can there be another financial crisis say, like the Great Depression?”

I was told:

“The odds are unlikely.”

I would have received a smarter response by shaking my Magic 8 Ball.

And yet. Still.

Why did I believe the bullshit?

Drink the Kool-Aid?

Live and learn. I’m sorry.

The mass assembly-line financial services firms still tout the curve.

And they’re going to seduce you with it again as this cyclical bull market rolls on. Fall for it and it’ll plant your money like a talking human right in the middle of “Ape City.”

“You cut his brain you damn, dirty apes!”

Don’t be a slave to the “normal” bell curve.

Here’s how to avoid the pitfalls.

Random Thoughts:

1). Realize you’re not rational which means markets aren’t either. First, my thought is, as people, we’re one breath away from becoming unglued like the crowds killing each other over $2 waffle irons at Wal-Mart during a black Friday midnight sale.

Here’s your bell curve: Rational investors on black Friday.

As systems are managed by people and we are emotional beings, panics can and will occur more frequently than a Gaussian Curve indicates. Much more. And how many financial disasters do you need before you’re ruined? Oh you know the answer. JUST ONE.

Per Benoit Mandelbrot (he was a math guru for good, not evil) & Nicholas Taleb, the 1987 stock market crash based on bell-curve finance was something that could happen only once in several “billion billion” years.

If my math is correct, disastrous years 1987, 1998, 2001, 2008 are a hell of a lot shorter in span than a billion billion years apart!

Per the curve and those who preach it, stock markets are estimated to blow up in hmmm, the year 3950?

Don’t be delusional like Zira overdoing the “Grape Juice Plus,” aka champagne.

2). Know the facts. Ed Easterling from Crestmont Research is a pro who debunks the validity of the bell curve and its application to stock market gyrations.

Ed provides return frequencies over 101 rolling ten-year periods. What does it mean and how does it destroy the bell curve theory?

The average return of the 101 periods is 10 percent. However, as Ed states “average rarely happens.” And the curve lives for the average.

Historic returns are “barbell shaped,” not “bell curved.” Plain to see.

If more returns circulated around the average, the blue bar would be more pronounced.

Stock market returns outside of the neat and tidy world the financial industry tried to create, tend to cluster and prices have a “memory” of sorts and gust like wind.

When you step back, it makes sense?

3). Where does your adviser stand? Ask the question. As an adviser, I can’t ignore the damn thing however I’m well versed in its pitfalls. Market price changes are more “messy.” Less bell curvy. Price movements are not as uniform as the curve outlines.

If your adviser believes hook, line and sinker in this curve, you’re going to lose your ass. Time for you to find another professional while times are good.

“Markets keep the memory of past moves, particularly of volatile days, and act according to such memory. Volatility breeds volatility; it comes in clusters and lumps. This is not an impossibly difficult or obscure framework for understanding markets. In fact, it accords better with intuition and observed reality than the bell-curve finance that still dominates the discourse of both academics and many market players.” Mandelbrot, Taleb.

4). Large market swings are NOT anomalies. Financial professionals and they’re clients are told to believe that large market swoons are rare – like as rare as Earth being overrun by smart, talking apes seeking to enslave you.

Listen, nobody can predict when a disaster is going to strike; being open to the fact that it can happen more often than once every 5 billion years is a fine start, however.

How Fractals Can Explain What’s Wrong With Wall Street.

Print the article from Scientific American. Send a copy to your financial partner for discussion.

You may be surprised (or shocked) by what you find.

Perhaps it’s your portfolio’s destiny to beware the curve.

Dr. Zira: What will he find out there, doctor?

Dr. Zaius: His destiny.

HA! Fooled ya!

HA! Fooled ya!